Compare Various MCLR Rates

*MCLR rates as of 7th Oct, 2019.

**For best UI experience on mobile, please flip the screen (Landscape view)

Compare the past trends in MCLR of any bank

| Bank | Bank Type | Overnight | 1 Month | 3 Months | 6 Months | 1 Year | |

|---|---|---|---|---|---|---|---|

| State Bank of India (SBI) | Public Sector Banks | 7.70% | 7.70% | 7.75% | 7.90% | 8.05% | |

| ICICI | Private Sector Banks | 8.20% | 8.20% | 8.25% | 8.40% | 8.45% | |

| Axis | Private Sector Banks | 8.10% | 8.10% | 8.30% | 8.40% | 8.45% | |

| Bank of Baroda (BOB) | Public Sector Banks | 7.95% | 8.05% | 8.15% | 8.30% | 8.35% | |

| Citi | Foreign Banks | 8.00% | 8.15% | 8.15% | 8.30% | 8.30% | |

| HDFC | Private Sector Banks | 7.95% | 8.00% | 8.05% | 8.15% | 8.35% | |

| IndusInd | Private Sector Banks | 9.00% | 9.05% | 9.35% | 9.50% | 9.55% | |

| Kotak | Private Sector Banks | 8.25% | 8.25% | 8.40% | 8.60% | 8.75% | |

| Yes | Private Sector Banks | 8.00% | 8.75% | 9.20% | 9.40% | 9.70% | |

| IDFC | Private Sector Banks | 8.85% | 8.85% | 9.00% | 9.15% | 9.30% | |

| DBS (Development Bank of Singapore) | Foreign Banks | 8.00% | 8.20% | 8.25% | 8.30% | 8.30% | |

| Dena | Public Sector Banks | 8.10% | 8.30% | 8.45% | 8.65% | 8.80% | |

| Bank of Maharashtra | Public Sector Banks | 8.15% | 8.25% | 8.30% | 8.40% | 8.50% | |

| Bank of India (BOI) | Public Sector Banks | 8.10% | 8.20% | 8.25% | 8.30% | 8.35% | |

| Oriental Bank of Commerce (OBC) | Public Sector Banks | 8.30% | 8.45% | 8.50% | 8.70% | 8.75% | |

| Punjab National Bank (PNB) | Public Sector Banks | 7.85% | 7.90% | 7.95% | 8.15% | 8.25% | |

| Punjab and Sind | Public Sector Banks | 8.10% | 8.25% | 8.35% | 8.45% | 8.50% | |

| Standard Chartered (SCB) | Foreign Banks | 8.30% | 8.95% | 9.30% | 9.30% | 9.35% | |

| UCO (United Commercial Bank) | Public Sector Banks | 7.85% | 8.00% | 8.10% | 8.35% | 8.45% | |

| Union Bank of India (UBI) | Public Sector Banks | 7.95% | 8.00% | 8.10% | 8.20% | 8.35% | |

| United Bank of India | Public Sector Banks | 8.00% | 8.25% | 8.40% | 8.55% | 8.70% | |

| Vijaya | Public Sector Banks | ||||||

| Andhra | Public Sector Banks | 7.90% | 7.95% | 8.15% | 8.30% | 8.40% | |

| Jammu And Kashmir Bank | Public Sector Banks | 7.85% | 7.95% | 8.20% | 8.50% | 8.70% | |

| HSBC | Foreign Banks | 8.10% | 8.10% | 8.25% | 8.35% | 8.45% | |

| Corporation | Public Sector Banks | 7.90% | 8.05% | 8.35% | 8.50% | 8.65% | |

| IDBI | Public Sector Banks | 7.85% | 8.10% | 8.35% | 8.50% | 8.85% | |

| Allahabad | Public Sector Banks | 7.90% | 7.95% | 8.20% | 8.25% | 8.40% | |

| Central Bank of India | Public Sector Banks | 7.75% | 7.90% | 8.00% | 8.15% | 8.25% | |

| Indian Bank | Public Sector Banks | 7.95% | 8.05% | 8.20% | 8.25% | 8.35% | |

| Indian Overseas (IOB) | Public Sector Banks | 8.05% | 8.20% | 8.35% | 8.40% | 8.50% | |

| Canara | Public Sector Banks | 8.15% | 8.20% | 8.30% | 8.40% | 8.40% | |

| Deutsche Bank (DB) | Foreign Banks | 8.30% | 8.75% | 9.75% | 9.75% | 10.25% | |

| BNP Paribas | Foreign Banks | 8.75% | 8.85% | 9.10% | 9.20% | 9.40% |

.

What is MCLR?

MCLR or Marginal Cost of fund based Lending Rate is the minimum interest rate below which commercial banks, generally, cannot lend to any customer. It is a determining factor set by the reserve bank of India for the lending rates of commercial banks and to replace the old base rate system. There could be few instances where banks could lend below MCLR rates. Such instances are very few and restricted to highly rated corporates who may need a very customized loan.

On the 1st of April 2016, RBI first implemented the MCLR based lending rate to determine the interest of different loans. MCLR is an internal benchmark rate which is decided by each bank from time to time, and accordingly, the banks have to calculate and levy interest on the loans they disburse. All the banks are required to publish their MCLR on website and generally it is updated by 7th of each month.

This was a much-needed change in the banking system for the benefit of the customers, especially for the SMEs and MSMEs and also for the individual customers. Earlier when RBI used to cut interest rates, the benefit of the same used to pass on to the customers after a long time. It is due to the inefficiency of the banking system which used to take long time to pass benefit of reduced interest rates to borrowers. With the introduction of MCLR, the financial institutes have to alter and adjust the lending rate accordingly as soon as there is any change in the repo rate.

Objectives Of MCLR:

- The primary objective of MCLR is to provide the benefits of a rate cut to the end customer as soon as the cut happens.

- To bring transparency in the determination of lending rates by commercial banks and other financial institutions

- To make it all fair for the lender and the customer by ensuring availability of loans at reasonable interest rates.

- To improve the worth of the lending institution and for bringing in healthy competition.

Generally, by 7th of each month, Commercial banks publish MCLR for different maturities of loans (time period like Overnight, 1 month, 3 months, 6 months, 12 months monthly, quarterly, etc.)

What is the relation between MCLR and final interest rate charged to the borrower?

Spread: It is the difference between the MCLR and the actual interest rate. It is the additional charge which you pay over and above the MCLR, and it varies from one loan type to another. For example, the MCLR for a one year home loan is 8.2%, and the spread is 0.3% so that the actual interest rate would be 8.5% on the home loan. The spread is fixed at the time of disbursal of the loan and only changed if there is a significant alteration in the borrower’s profile. ( would spread not be charged for different risk profiles?, please check seems factually inaccurate)

Credit linked spread can be negotiated and can vary from bank to bank and borrower to borrower. Borrowers with high credit rating and good track record could negotiate for a small spread. For average borrowers, the spread could be about 1%

What is Base Rate?

Base rate was a conceptualised before 1st of April 2016. Base rate is also the minimum interest rate at which the banks lends money to the customers. for all fixed rate as well as floating rate loans. Under this regime, the bank used to lend at lower interest rate even lower than the base rate to its employees, premium, or favorite customers, which was an unfair practice and affected general customers.

These days most commercials banks are pricing loans linked to MCLR and not base rate. Cooperative banks still use base rate.

Which loans are linked to the MCLR rate?

Banks are free to offer fixed rate loans or floating rate loans. In fixed rate loan, the interest rate is fixed for the period of loan and does not change. In floating rate loans, the applicable interest rate changes with changes in benchmark. The benchmark could be MCLR or any other one like GSec interest rate, T Bill rate or CP rate.

Most commercial banks are offering every possible loan – working capital, long term loan, loan for buying equipment etc – linked to MCLR.

How to choose the right bank and right MCLR tenor, while switching bank or taking a new loan ?

Either chose banks which do not change MCLR much either when RBI is increasing interest rates or when RBI is reducing it OR chose banks which actively reduce interest rates when RBI is reducing the same. This is also called transmission effect.

What is MCLR reset frequency?

The reset frequency of interest rate determines which Marginal cost of fund based lending rate(MCLR) will be used to finalize the interest rate on loan. So, if the reset frequency of a home loan is set to 3 months, then the MCLR of 3 months benchmark will be in use, and similarly, for a 1-year reset frequency, 1-year MCLR will be used as the benchmark to determine the loan interest rate. Since every MCLR of the different tenor is different, the interest rate changes with the MCLR as well.

How will a change in repo rate affect Marginal Cost of Funds based Lending Rate(MCLR)?

When RBI changes Repo Rate, the same is reflected in MCLR. If the repo rate is slashed down, the MCLR is also reduced down and vice versa. The amount of change in MCLR is not same as change in repo rate. Generally it is much smaller and the amount of change could also vary from bank to bank

To remove the effect of funds based lending rate, now it is compulsory to link even the base rate loans to MCLR. Home Loans, Personal loans etc are all impacted by MCLR. The only loans which are not under this regime –

- Loans to employees of the bank

- Government’s loans schemes like Jan Dhan Yojana

- Fixed rate loans

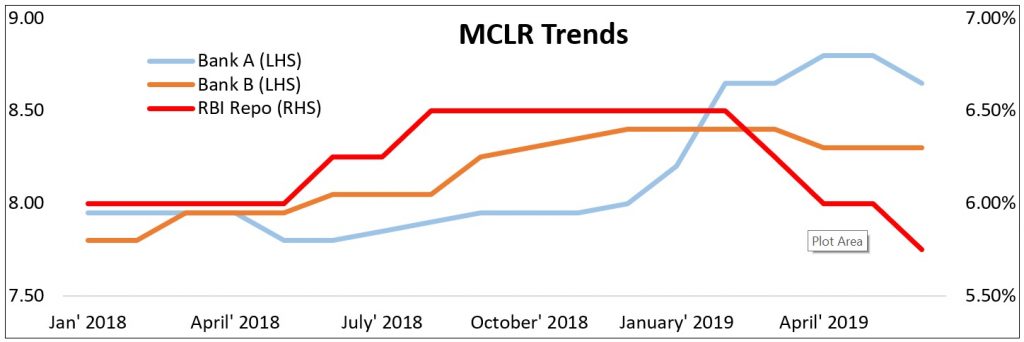

Using MCLR trends of past years to chose from which bank to borrow

Edugains’s MCLR trends tool:

Edugains’s MCLR trends tool can help you analyse past Marginal Cost of Fund Based Lending Rate(MCLR) trend of various private, public or foreign banks together on 1 screen so that corporate can compare and identify the increase or decrease trends in MCLR over the past 12-18 months.

MCLR trends can help in the decision of choosing the right bank and right tenor. A bank with relatively lesser MCLR may increase its MCLR more sharply when RBI increases repo rate and in long run turn out to be more expensive. Therefore a bank which increases its MCLR and also reduced the same in line with RBI’s interest rate movement would be ideal bank.

In the example below MCLR are linked to repo rate. Banks MCLR are plotted on the left hand side and RBI rate is plotted on the right hand side in the chart below. Over the period of time as RBI has revised the repo rate and these banks have changed their MCLR accordingly. Bank A has increased their MCLR more than Bank B, So on Jan 2018 with help of our MCLR trends tool the borrower could have identified that although Bank A is beneficial for shorter time span but over the longer time span Bank B would have been the right choice.

Is low MCLR a reason to choose the bank?

Have free Q&A with our banking experts or Check out the MCLR FAQs

Frequently asked questions

Can banks lend below MCLR?

Yes, banks can lend below MCLR. For customers on whom banks have good credit comfort, they may choose alternative benchmark and lend below MCLR.

How do I understand MCLR in layman’s language?

MCLR stands for Marginal Cost of Funds based Lending Rate. In simple terms, it is a rate at which a bank can lend and earn an acceptable return on equity. MCLR differs from bank to bank and from period to period. Banks have to publish MCLR on their website by the first week of every month.

Is it important to choose correct MCLR – 1 month vs 3 months vs 6 months vs 12 months?

You must understand which MCLR suits your business or ongoing market trend and ask for that. Not necessarily, the MCLR chosen by bank is best for you.